What the next decade of AI look like when you stop listening to the people building it

We have seen this before.

Not AI specifically. But this. The arrival of a technology so genuinely powerful that it could restructure everything — who holds power, who creates value, who gets left behind. The moment when the architecture of human civilisation is briefly, genuinely, up for renegotiation.

We saw it with the printing press. The internet. Crypto.

And every single time, the same thing happened. The technology that could flatten the hierarchy was captured by the people at the top of it before anyone else understood what was occurring. Not through conspiracy. Not through malice. Through the oldest and most reliable force in human history — the people with existing capital, existing infrastructure, and existing power moving faster than everyone else because they had more resources to move with.

AI is not different.

AI is the most extreme version of that pattern ever attempted. And it is already well underway.

WHAT IS ACTUALLY HAPPENING RIGHT NOW

Strip away the press releases, the safety manifestos, the breathless announcements about capabilities. Look at the structural reality.

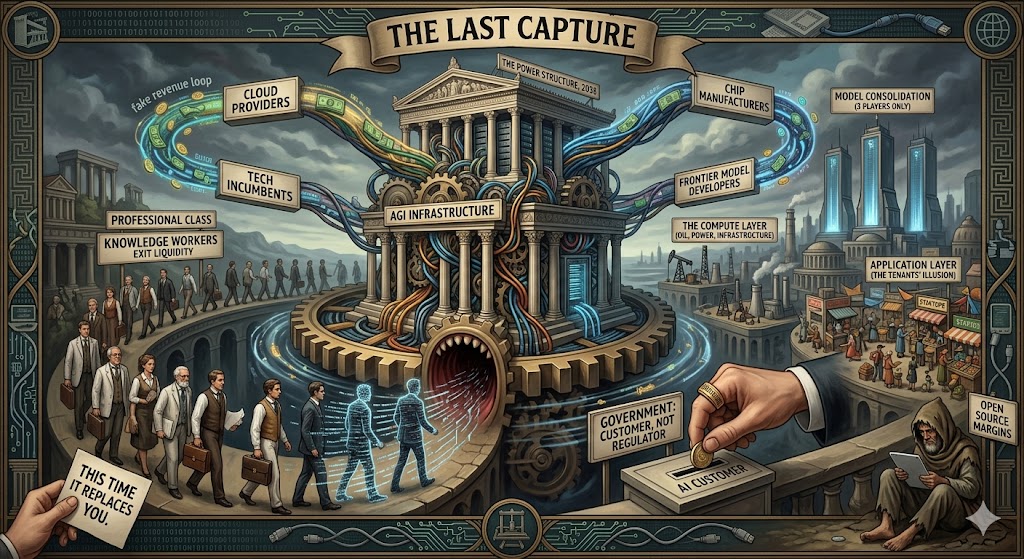

OpenAI and Anthropic now sit at the centre of nearly $2 trillion in future cloud revenue committed by Microsoft, Amazon, Google, and Oracle. The mechanism is almost elegant in its circularity. A tech giant writes a billion-dollar check to an AI startup. The contract requires that money to be spent back on the giant’s cloud infrastructure. The cash never actually leaves the building. The giant books the consumption as commercial revenue. The startup books the investment as runway. Both companies report growth. Neither has actually created new value — they have recycled existing capital through a loop that looks like an economy but functions like an accounting exercise.

OpenAI’s annualized cloud bill has reportedly exceeded $60 billion. Its actual revenue sits closer to $25 billion. Anthropic spent $2.66 billion on Amazon Web Services in nine months — roughly every dollar it earned, straight back to its investor.

The entire AI boom, at its financial core, is four companies paying two companies with money those two companies spend back on the four companies. And the valuation gains from each round of funding inflate the paper assets of the investors who funded the previous round.

This is not the internet. The internet created genuine distributed value — anyone with a connection could reach anyone else, build anything, publish anything. The infrastructure was cheap enough that a teenager in a bedroom could compete with a corporation.

AI infrastructure is the opposite. Training a frontier model costs hundreds of millions of dollars. Inference at scale costs billions annually. The data centres required are measured in gigawatts of power consumption. The compute is controlled by three companies — Nvidia for chips, and the hyperscalers for everything else.

The barrier to entry is not a regulatory moat or a network effect. It is physics. You cannot train a frontier AI model in a garage. The democratisation of AI that the press releases promise is real at the application layer — anyone can use the tools — and completely fictional at the infrastructure layer, where all the actual power resides.

The revolution is available as a subscription. The means of revolution are owned by the same people who owned everything before it.

THE FAKE REVENUE LOOP IS THE LEAST OF IT

The financial circularity matters. But it is not the most important thing happening.

The most important thing is what AI actually does to the structure of labour and value creation — and who benefits from that restructuring.

Almost 49% of jobs can now use AI for at least 25% of their tasks. Employers predict 34% of all work tasks could be fully automated by 2030. Wall Street banks have internally planned to eliminate approximately 200,000 jobs over the next three to five years, specifically in entry-level and back office roles. In just the first six months of 2025, nearly 78,000 tech jobs were directly tied to AI-driven layoffs.

And here is the part that inverts everything people assumed about automation:

Previous waves of automation displaced blue-collar workers. Factory hands. Assembly line operators. People without degrees doing physical, repetitive work.

AI primarily displaces educated, white-collar labour. The people who thought they were safe because they had degrees and knowledge work and careers rather than jobs. Legal associates. Junior analysts. Copywriters. Programmers at the mid-level. Radiologists. Customer success managers. The entire professional class that the economy spent fifty years training and credentialing and promising security to.

The displacement isn’t visible yet in the aggregate numbers because companies don’t advertise automation as the reason for restructuring. They call it efficiency. Reorganisation. Strategic realignment. The real number of AI-displaced or AI-foregone positions in 2025 is estimated at 200,000-300,000 — roughly four to five times the officially reported figure.

This is the deliberate opacity of predatorialism operating at scale. The extraction is happening. It just isn’t being named.

THE POWER STRUCTURE THAT IS BEING BUILT

Here is what the next twelve years actually produce if the current trajectory holds — which it will, because no force currently in existence is strong enough to alter it significantly.

The compute layer becomes the new oil.

Nvidia, the hyperscalers, and whoever wins the next generation of chip architecture will control the infrastructure that everything else depends on. This is not a technology company story. It is a resource extraction story. The companies that control compute in 2035 will have the kind of structural power that oil companies had in 1975 — with one critical difference. Oil could be found in inconvenient places controlled by inconvenient governments. Compute consolidates naturally toward whoever has the most capital to build data centres and the most political influence to secure the energy supply to run them.

The model layer consolidates to three.

OpenAI. Google. Anthropic. Possibly one Chinese competitor. That is the frontier model landscape in twelve years. Every smaller lab either gets acquired, runs out of money, or finds a niche application layer where they can survive without competing at the frontier. The economics of frontier model development make this mathematically inevitable — the compute costs scale faster than the revenue for anyone not already at hyperscale. The market structure that emerges looks less like software and more like aerospace. Three or four players globally. Enormous barriers to entry. Governments deeply intertwined with the survivors because they cannot afford for any of them to fail.

The application layer creates the illusion of competition.

Ten thousand startups will be built on top of the three frontier models. Most will fail. Some will create genuine value. A handful will become very large businesses. This layer will look vibrant and innovative and competitive — and it will be, within the constraints of the infrastructure it depends on. Every application company is a tenant. The landlords are the frontier model providers and the hyperscalers beneath them. When the landlord decides to build a competing product — and they always decide — the tenant finds out what their lease was actually worth.

Governments become customers, not regulators.

This is the most consequential shift and the least discussed. Governments need AI for defence, intelligence, healthcare administration, tax collection, social benefit management, border control, and a hundred other functions that have become too complex and too data-heavy for human-scale management. The countries that fall behind on AI capability fall behind on national security in a way that is not recoverable on a political timescale. This means every significant government on earth becomes a major customer of the three to four frontier model providers. And customers do not meaningfully regulate their critical suppliers. They negotiate. They request. They occasionally threaten. But the leverage flows in both directions, and the company that controls the AI your military depends on has a different kind of relationship with your government than a company that makes widgets.

The EU tried to regulate AI with the AI Act. It produced compliance theatre and pushed serious AI development further toward American and Chinese providers. MiCA for crypto was the dress rehearsal. The AI Act is the main event. The outcome will be the same — rules that incumbents can absorb and smaller competitors cannot, effectively licensing the existing power structure into permanence.

THE AGI QUESTION — AND WHY IT ALMOST DOESN’T MATTER

Every serious AI lab CEO has now stated publicly that AGI — artificial general intelligence, systems that match or exceed human cognitive performance across all domains — is coming within years, not decades.

Sam Altman: arriving this decade, possibly this half of it. Demis Hassabis: multi-year horizon, not already here. Prediction markets in April 2026: 55% probability OpenAI achieves AGI by 2030.

The honest answer is that nobody knows, including the people building it. The benchmarks that were supposed to be AGI-hard keep falling faster than expected. The researchers who designed them keep moving the goalposts because the alternative — admitting that something important has already happened — is too disorienting to process cleanly.

But here is the thing that almost nobody says clearly:

Whether AGI arrives in 2028 or 2038 doesn’t change the fundamental power structure question.

The question is not whether the technology reaches human-level capability. The question is who owns it when it does. And that question is already being answered, right now, through the capital structures and infrastructure lock-ins and government dependencies being built while everyone is still arguing about capability timelines.

If AGI arrives in 2028 and it belongs to OpenAI, which belongs functionally to Microsoft, which has a $600 billion backlog tied to it — then AGI is a Microsoft product. With a terms of service. And a pricing model. And an enterprise sales team.

The most transformative technology in human history, if it arrives on the current institutional trajectory, will be released as a SaaS product with tiered pricing and a 99.9% uptime SLA.

The revolution will have an API.

THE GOOGLE TRAP AND WHY IT MATTERS

There is a specific dynamic playing out right now that tells you everything about how the next twelve years resolve.

Google has the best AI infrastructure on earth. It owns the chips, the data centres, the distribution, and decades of the most valuable training data ever assembled. On every structural metric — compute, capital, talent density, distribution reach — Google should be winning.

It isn’t. OpenAI has the narrative. The momentum. The cultural presence. The thing people mean when they say AI.

And Google, the company that should own this transition by right of infrastructure, is losing the story to a startup that spends $60 billion a year on compute it can barely afford — $35 billion more than it earns.

This matters because it demonstrates something important about how AI capture actually works. It isn’t purely about who has the best technology or the deepest infrastructure. It’s about who moves fastest to embed their product in the places where it becomes impossible to remove. Enterprise contracts. Government dependencies. Developer ecosystems. The psychological default of what “AI” means to a generation of users.

OpenAI is losing money at a scale that should be fatal. It is surviving because the people who would benefit most from it failing — Google, Microsoft, Amazon — are also the people funding it, because none of them can afford to let someone else own the category. The incumbent is paying for the disruption of itself because the alternative is losing the disruption to a third party.

This is a new kind of market structure. Not competition. Not monopoly. A cartel of mutual dependencies where every player is simultaneously the other’s investor, customer, competitor, and existential threat.

THE LABOUR QUESTION IS THE CIVILISATIONAL QUESTION

Everything above is the power structure story. The infrastructure capture. The capital dynamics. The government dependencies. The AGI race.

The labour story is different. And it is the one that actually determines what the next twelve years feel like for most people.

The displacement is not coming. It is happening. The reason it doesn’t feel like a crisis yet is that it is distributed across millions of individual hiring decisions that are never publicly attributed to AI. The company that simply doesn’t backfill the role when someone leaves. The bank that processes fifty percent more loan applications with thirty percent fewer analysts. The law firm that produces twice the contract volume with the same number of junior associates. The displacement is in the negative space — the jobs that don’t get created, the careers that don’t exist, the entry-level positions that were always the training ground for senior positions and are now automated away before the next generation can use them as a ladder.

This creates a specific kind of catastrophe that the GDP numbers will not capture for years.

The people being displaced are not the bottom of the economic hierarchy — they are the middle. The credentialed professional class. The people who followed every instruction the system gave them, accumulated the debt the system required, and arrived at the career the system promised. AI is not disrupting the already precarious. It is disrupting the people who thought they had made it.

And the gains from that disruption flow almost entirely upward — to the shareholders of the companies deploying AI, the owners of the infrastructure it runs on, and the small number of people skilled enough to direct the systems rather than be replaced by them.

This is predatorialism’s final form. Not extraction from the obviously vulnerable. Extraction from the people who thought the deal they made with the system was honoured. Who thought their education was their protection. Who thought knowledge work was safe.

It turns out knowledge work was safe only until knowledge could be automated. And knowledge can now be automated.

THE NEXT TWELVE YEARS — WHAT ACTUALLY HAPPENS

2026-2028: The embedding phase

AI becomes invisible infrastructure at the same speed that electricity did. Businesses that don’t integrate it can’t compete with businesses that do. The cost pressure is too severe and too immediate. This is not optional adoption — it is survival pressure. The embedding happens faster in white-collar industries than anywhere else, because those are the domains where the productivity gains are most immediate and most measurable. The job market for entry-level knowledge workers deteriorates sharply. The reported unemployment numbers stay relatively stable because the displacement happens through hiring freezes and role elimination rather than mass layoffs. The human cost is real and large and mostly invisible in the statistics.

2028-2030: The consolidation

The frontier model market settles into its permanent structure. Three or four providers. Everyone else is building applications on top. The AGI debate reaches some form of resolution — either a system arrives that is genuinely impossible to deny or the goalposts move again in a way that becomes philosophically untenable. Government dependencies on AI providers become structural. The first major geopolitical crisis involving AI capability asymmetry occurs — not a science fiction scenario, just a situation where one country’s AI-enhanced military or intelligence capability produces an outcome that would not have been possible two years earlier. The regulatory response globally is nationalisation of AI infrastructure in some countries and deeper entrenchment of incumbents in others.

2030-2035: The two AIs

The same bifurcation that happens to crypto happens to AI.

The first AI is fully integrated into institutional life. Healthcare. Finance. Government. Education. Law. It is invisible, reliable, deeply embedded, and controlled by the same three or four companies that built the infrastructure. Most people interact with it dozens of times a day without knowing it. It is profoundly useful and profoundly concentrated in its ownership. The value it creates flows primarily to the shareholders of the companies that own it.

The second AI exists in the open source margins. Models that anyone can run. That no one company controls. That governments cannot easily shut down. Smaller than the frontier systems. More capable than anything that existed five years earlier. Used by people who cannot afford or do not trust the institutional layer. This is where the genuinely interesting things get built — not because the technology is better but because the constraints are fewer and the incentives are different.

The open source layer is where the original internet energy went. The institutional layer is where the money went. Both exist simultaneously. They serve different masters.

2035-2038: The AGI moment and what it actually means

If AGI arrives on something like the current trajectory — and prediction markets say there is a majority probability it does before 2030 — the immediate experience of it will be nothing like the science fiction.

It will not be a single announcement. It will be a gradual crossing of a threshold that nobody can agree was crossed until years later. The systems will keep getting more capable. The benchmarks will keep falling. The goalposts will keep moving. And at some point — probably already past — something will be operating in the world that is qualitatively different from what came before it, without anyone having pulled a lever or flipped a switch.

What it means practically is not the end of human work. It is the end of human work as the primary source of human economic value. The productivity gains from systems that can do most cognitive tasks better than most humans go somewhere. They go to the owners of the systems. Which is to say they go to the same people and institutions that already hold most of the capital.

The prediction markets will move. The AGI ETF will launch. Sam Altman will post something. And then the world will be more unequal than it was the day before, in a way that is structurally different from any previous form of inequality — because previous inequality was about who owned the land, or the factories, or the data. This inequality is about who owns the thing that can do everything the rest of us were paid to do.

WHY IT DOESN’T HAVE TO BE THIS WAY — AND WHY IT WILL BE ANYWAY

There are genuine alternatives. Not fantasies. Real structural choices that societies could make.

Compute could be treated as public infrastructure, like roads or electrical grids — owned collectively, accessed by everyone, priced at cost rather than at extraction. The AI Act could have teeth rather than compliance theatre. Open source models could be actively supported by governments rather than viewed as a security threat. The productivity gains from AI could be redistributed through mechanisms that don’t require everyone to become a prompt engineer.

None of this will happen at the scale required. Not because it’s impossible. Because the people who would need to do it are the same people who benefit most from not doing it. The regulatory capture happened before the regulation was written. The government dependencies were built before the governments understood what they were depending on. The infrastructure lock-ins were signed before most policymakers understood what infrastructure meant in this context.

We have been here before. Printing press. Industrial revolution. Internet. Every time, a brief window when the architecture was genuinely up for renegotiation. Every time, that window closed faster than the people who wanted a different outcome could organise to claim it.

The window for AI is closing now. Not slammed shut — still open a crack. But closing.

The ideology of the people building it — genuinely, not cynically — is that the technology is so beneficial that its concentration is a temporary and acceptable cost. That the rising tide will lift all boats eventually. That the transition pain is real but the destination is worth it.

They may be right about the destination. They are almost certainly wrong about who gets to live there.

WHAT THIS MEANS IF YOU ARE WATCHING

Not if you are an investor. If you are a human being watching this happen in real time.

The framework that served for crypto applies here too, with one critical difference. Crypto’s capture was bad for idealists and good for institutions. AI’s capture is bad for idealists, good for institutions, and existential for the professional class that has no idea it is the exit liquidity for this particular trade.

The people who will navigate the next twelve years best are not the people who understand AI most. They are the people who understand power most. Who can read structural capture when it is happening. Who know that the tool being placed in their hands is genuinely useful and simultaneously designed to extract from them.

Use the tools. They are real and they are powerful and the productivity gains are genuine. But do not confuse being given access to a tool with owning the means of production. Every factory worker in 1905 had access to industrial machinery. That access did not make them industrialists.

The technology is extraordinary. The application of it to human flourishing is real. And the ownership structure being built around it will concentrate the gains from that flourishing in fewer hands than any previous technological revolution in history.

Because this time the technology doesn’t just replace physical labour or routine cognitive labour.

This time it replaces the thing that the broadest possible range of humans were paid to do.

And the people who own it are not going to share what that is worth.

Not because they are evil.

Because we are us.

And we never do.